What we learned by closing a $4M investment from Accel

I’m pleased to share the news that Altinity has raised a $4M seed investment from Accel. Dan Levine led the round. We are honored by Accel’s trust and delighted to work with Dan. We plan to use the investment to roll out our new Altinity.Cloud platform and to strengthen ClickHouse® into the best analytic database on the planet.

Dan was the first venture capitalist to contact us, as he tells in his blog article about the seed investment. He was enthusiastic but also very patient.That was fortunate, because we then talked to 43 other VCs at greater or lesser length over the next year and a half. The count omits those who greeted our overtures with stony silence. In the end we were absolutely confident Dan and Accel were the right choice. At the same time, we learned from many others.

Looking back, it is apparent we did more than just collect a check from a great investment team. We also learned a number of valuable lessons about early stage venture investment. Many of these were not obvious, at least to me. In this article I will share what we learned, along with a spreadsheet we developed to help with investment math. I hope our account will be useful — or at least entertaining!

What do VCs really want?

VC websites often sport brave slogans like “we are looking for bold entrepreneurs who will change the world.” What they are actually looking for, of course, is far more concrete: a big return on a speculative bet about a new business. The first thing we learned was how venture capital actually works and how we fit in.

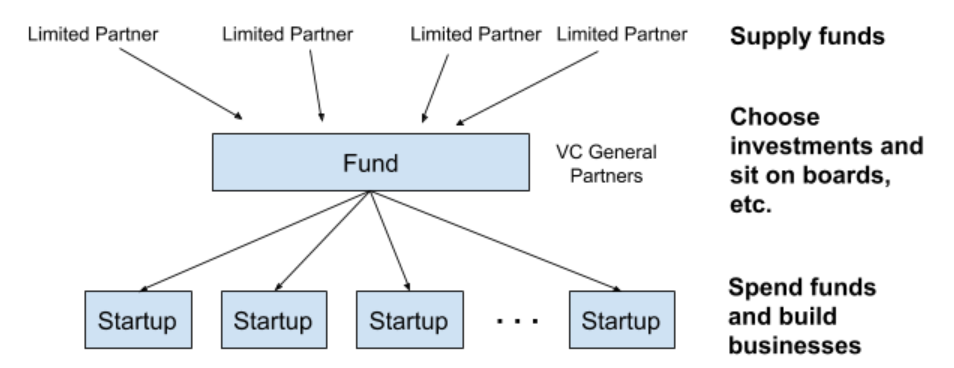

Let’s start with where the money comes from and how it is managed. Venture capital firms operate one or more funds, which they use to make investments. Each venture capital firm has general partners who work for the company, decide where to invest, and take care of serving on boards and other duties required to supervise each investment. There is also another type of partner, known as a limited partner or LP. LPs can be wealthy individuals, pension funds, sovereign investment funds, you name it. They supply cash but have no role in making investment decisions. Here is a picture.

In the first meeting with a new VC you typically hear about the current funds, how big they are, and other details like reserves for follow-on investments in promising companies. When you ask what payback they are seeking the most frequent answer is “return the fund.” This is so common that I stopped writing it down unless the answer was something different. It means the investment in your company needs to pay out at the value of the entire fund, not just what the VC put into your company. The reason has to do with the mechanics of the funds.

Most startups fail or return money that does not come close to covering the investment. To provide a decent return to limited partners and VC general partners plus pay overhead, at least a couple of investments need to hit home runs and to pay off at full value of the fund. It’s basic math, but the numbers are big. Say a $400M fund invests $40M total for a 25% share of your startup, a typical target percentage. To return the fund means that the startup will have to exit for $1.6B ($400M = $1.6B * 25%). Grand slams like Snowflake return far more and make the fund very successful.

At first it was disconcerting when A-list VC prospects baldly asked how we would get them an exit in the $1B+ range. Over time I developed empathy for this attitude. VC general partners have to make the math work or find another job. Meanwhile entrepreneurs need to have a problem that fits the pattern of investment or venture funding does not make a lot of sense. That’s the economic reality and has little to do with how individual VCs feel about you personally, or even about your business.

We needed to articulate to ourselves how we would win in a large market–SQL data warehouses–filled with a lot of savvy competitors like Amazon and Snowflake. The classic strategy is to create a new market that did not previously exist, then become the leader. Anurag Gupta and his colleagues at Amazon put it brilliantly in a paper on Amazon Redshift:

Our goal with Amazon Redshift was not to compete with other data warehousing engines, but to compete with non-consumption.

The unique differentiation of ClickHouse is that it is open source and runs anywhere: from public clouds down to Android phones. Any developer on the planet can download it and add high performance analytics to any application without sacrificing portability or scaling. That’s an enormous expansion of the market that will fuel innovation not just at the database level but will extend to new applications of big data as well as the tools and platforms to run them.

Here’s another key insight: it took months to be able to state that value proposition in three sentences. It’s like learning a new language — anyone can learn to say hello but achieving fluency requires real work.

We did a lot of modeling to understand the growth trajectory needed to achieve the kind of revenue our predecessors are making. One of the conclusions was that we needed to build a great cloud platform for ClickHouse. It’s a tried-and-true way to build a successful business, especially for companies that manage data, and one that our customers have confirmed as a fruitful path to growth. We believe in the plan and it matches venture capital economics.

VCs Work Off a Thesis

I didn’t know a lot of early stage VCs when we began fund-raising, though like everyone I heard they were fine human beings worthy of acquaintance. The initial conversations were illuminating in one particular respect. Venture capitalists don’t necessarily know that much about specific technology or markets.

Here’s an example. My favorite demo for ClickHouse is the ClickHouse-fast demo where I first run a query on data generated purely in memory followed by a similar query that accesses 1.3 billion rows of taxi data in slowish network-attached storage. I usually pause dramatically after the in-memory query to ask which query is going to be faster. Everybody knows access to memory is faster than storage, right?

Actually, in this demo it’s not. You have to be very careful to make an apples-to-apples comparison when comparing memory and storage access speeds. ClickHouse compresses stored data and parallelizes I/O extremely well. Reading from storage is therefore very fast. With ClickHouse it is not hard to choose in-memory queries that look similar but run far slower because they have a different execution path with less parallelization or other inefficiencies. It’s a subtle point that experienced database people understand, whereas VCs I talked to often got it wrong. (And then argued about it, too.)

This experience illustrates that deep dives on technology are not always the best way to evaluate early stage businesses. Good VCs tend to look for proxies that indicate signs of traction. In our case Dan Levine knew about ClickHouse because his other start-up investments used it. Dan pays really close attention to things they like. Dan picked up on ClickHouse earlier and more clearly than anyone we spoke to. The fact that we were an experienced team already selling services profitably was perhaps another useful signal. But Dan was also looking for more than just specific signals–he was looking for a pattern related to data, backed by a solid team.

Over time, we found that the VCs who really picked up on our story had a thesis about the value of combining two things:

- Data – Faster and more cost effective ways of analyzing large datasets are inherently valuable to enterprises.

- Open source – There are standard models for marketing and monetizing open source projects to build very large businesses

VCs with these convictions tended to like what we were doing overall, though they often found specific things they didn’t like: open source community too small, too much competition, not the right team, already made a competing investment, etc. That said, we didn’t argue about the size of the market or whether open source was the right overall strategy to reach it. It helped that the original developers of ClickHouse at Yandex did an amazing job of open sourcing the code and starting a great community around it.

Not surprisingly, we learned that those same investors were precisely the people we wanted backing the company. Not only did we share key assumptions about the business, but they had funded such businesses before with successful outcomes. Because of that they could offer useful advice on big topics like strategy to build open source communities or workable business models. They could also connect us with outstanding people like Mike Olson of Cloudera (and many others) who had worked through similar problems and could help us see around corners.

Here’s a final insight that relates back to the technology point I made above. VCs can identify promising companies, but they can’t tell you how to run yours. As an entrepreneur you understand the technology, your customers, and what is feasible to achieve. We had a number of debates with potential investors about details of the business plan.

For example, many VCs favor pure cloud services, because the best ones experience explosive growth and high margins. However, a push-button service is not a complete solution, especially for complex enterprise products like databases. Altinity has been in business since 2017 and we have articulate users who say they want us to take care of running ClickHouse in the cloud. They also want application tools, new server features, training, support, and implementation help. Their problem is not just to deploy a database but to create applications that add value to their own business. If you help them do that you have a much more competitive business.

Our mission is to help any enterprise that uses ClickHouse. We provide everything customers need to be successful with ClickHouse, including a great cloud service. We also support the ClickHouse community to help ensure it becomes a permanent feature of the database landscape. Altinity is not just a cloud company.

What’s your weak point?

One of the things about presenting business plans to VCs is that you get insightful comments from smart people who have been around many successful startups. Actually, they probably don’t view the comments as especially insightful. VCs hear a lot of pitches and get practice picking off standard weaknesses.

One particular weakness for us was marketing. Our team is engineering heavy, and though we value sales highly none of us had a particularly strong background in marketing. One of our board members and founders, Peter Zaitsev, is a very savvy marketer on open source communities who regularly provides us practical advice. He also has a full time job running Percona. We needed to sort this out ourselves.

VCs who understood open source gave consistent feedback that we needed to think more about building the community and marketing to it, as well as what it would cost. That drove us to pay more attention to our own struggles creating enough leads to feed sales–we understood this was a problem but did not have a clear strategy to deal with it, nor had we budgeted accordingly. Basically they pointed out the strategic problem we were already wrestling with at a tactical level in sales calls. There were also helpful suggestions about how to fix it.

The most useful feedback came from a VC I knew from years earlier when he was an executive in the database industry. In just a few words he explained that marketing is a spectrum that runs from product marketing (figuring out product fit for customers) to demand generation (telling people about the product in a way that gets them to buy it). Companies need to decide where they are on the spectrum and invest accordingly.

This is probably obvious to a lot of readers but the scales fell from my eyes when he pointed this out. Successful open source projects like ClickHouse almost by definition get product fit right because the community fixes tend to address real problems. Building open source businesses is therefore very much about generating demand — building the community and getting people interested in buying. That was exactly the task that was giving us such headaches.

Not surprisingly, our first hire after closing the investment was a great demand generation person, Stephanie McArthur.

What’s the real cost of giving away equity?

The closer we got to accepting an investment the harder we looked at how much we were giving away and what we were going to get for it. Our founding team bootstrapped Altinity from zero, and we feel a strong sense of ownership. We evaluated options ranging from continued bootstrapping to non-dilutive loans to convertible notes and SAFEs to priced equity. We read and debated the article “Why Startups shouldn’t use YC’s Post-Money SAFE,” as well as many others. We had knock-down team arguments about funding trade-offs, including one on a rainy evening in a restaurant in Amsterdam. (I’m really sorry if you were sitting next to us.)

However you get there, it’s essential to examine carefully the cost and benefit of any transaction that involves equity. The article I just cited describes bad outcomes from using SAFEs, but the bottom line is that you can get in trouble with any type of financing if you don’t do the math on your equity capitalization, which is also known as the cap table. I was astonished to learn that a lot of entrepreneurs don’t do this.

The book “Venture Deals: Be Smarter Than Your Lawyer and Venture Capitalist” by Brad Feld and Jason Mendelson is a great introduction to how VC financing works and how to negotiate. It does not, however, explain investment math outside very simple examples. We looked for existing models and could not find anything that fit our case. Taking investment dilutes your shares but gives you the ability to make them more valuable. We needed something that could show outcomes from seed stage onwards to see the ratio under different paths.

We therefore built our own model to track cap table holdings through Series C. The cap table consists of shares, from which you can value holdings and compute percentages of ownership. It computes complexities like dilution due to employee share pools, pro rata investment rights, and liquidation preferences. All of these were things we wanted to understand and account for.

The resulting spreadsheet would do any accountant proud. In fact, that is a very useful insight all on its own. Investment math is complex, and the English language is a weak medium to describe it. Through building the spreadsheet we understood investment outcomes far better and could also experiment with many different scenarios. Here’s another helpful trick: ask each VC to provide a spreadsheet showing what he or she believes the cap table will look like after an investment. Dan Levine did exactly that, which made us confident that we and Accel were saying the same thing.

In the spirit of open source we are releasing a sample of the model. (Here’s the link). It was developed by my colleague Mindaugas Zukas. Based on our experience, I would say you will get the best value if you use it as a jumping off point and develop a new model that fits your circumstances. There are other models available on the Internet — including for-pay services. You can use them to test part or all of your calculations. By the time you get it working you’ll understand as much or more equity math than we do.

Thinking over our entire experience with the investment, we learned a couple of final lessons about financing in general and which path to take. Here’s my take on how to think through whether an investment makes sense.

- Take investment if you think it will make your shares more valuable. This is the flip side of the “return the fund” math VCs labor under. It’s hard to assess without constructing a model that runs through a few rounds of investment to an exit. Don’t just think about venture investment. Consider boot strapping, friends-and-family loans, etc. They can be far better ways to build a company depending on your capital needs.

- Give away as little equity as possible for the highest price. This is of course obvious, but doing it when you are uncertain about the exchange of value is hard. It is psychologically much easier to negotiate if you run the numbers and see the exact effect of an investment in dollars and cents. Don’t forget to calculate how much the business actually needs and use that to guide what you sell. It is way too easy to give away something you don’t fully understand.

For anyone who is interested, we went with a SAFE. The math worked out the same as other options, and it had fewer strings attached than, for example, an equity offering. I’m glad we did that, because it gave us more freedom to address issues related to growing the business.

Epilog

Returning to the initial paragraph of this article, we’re delighted to have Accel as a partner and are working to put their investment to good use. I should also mention that when COVID-19 arrived in earnest in March 2020, we were holding a term sheet signed by Dan Levine but had not closed the investment. We actually closed several weeks later. It is a credit to Accel that they followed through without question.

Closing a seed investment, even from an A-list venture firm, is just one step on a long journey. I don’t want to make it more than it really is. We learned some great lessons but still have a big job ahead of us. There’s a huge opportunity for our customers if they can get fast answers from the enormous datasets their businesses generate. ClickHouse is an outstanding analytic database that is on the way to equaling or exceeding every competitor. Open source allows us to put ClickHouse in the hands of every developer on the planet. It’s the kind of synergy that fuels revolutions in technology and we are excited to be on the next step to making it happen.

Every now and then you get a chance to hit the ball out of the park. Altinity is one of them. We look forward to working with the open source community, our customers, and our investors to lead the next wave of innovation in analytic databases. Contact us at info@altinity.com if you would like to join the adventure.

ClickHouse® is a registered trademark of ClickHouse, Inc.; Altinity is not affiliated with or associated with ClickHouse, Inc.

Thank you so much for this article! It has really helped me with my seed raise. Very kind of you to share your cap table which I’ve copied over to my GDrive. Thanks to superb founders like you who are paying it forward to help startups like mine, it has saved me a lot of time.